“If you don't have help from the Bank of Mum and Dad, it's almost impossible to think that you're ever going to get on the property market.”—Dr Kate Lycett, Australian Unity Wellbeing Index lead researcher, Deakin University

Key points

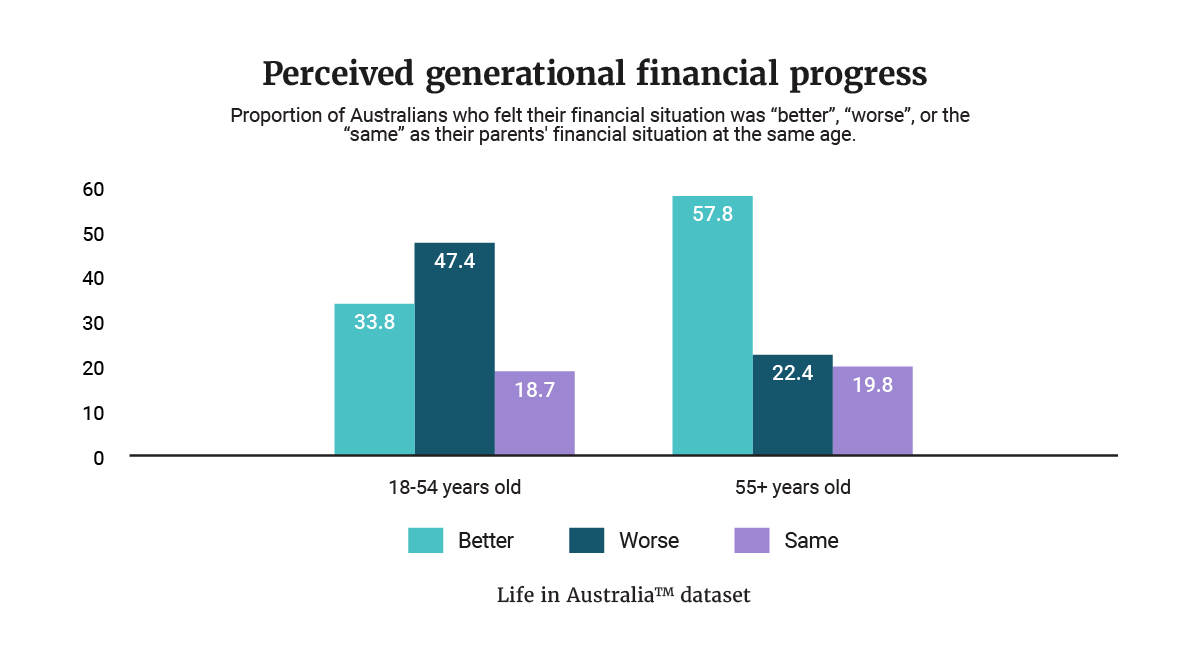

- Half of Australians aged 18 to 54 feel financially worse off than their parents, compared to just 20 percent of people aged 55-plus.

- Younger Australians are also more likely to put off paying for essentials, and are less satisfied with their ability to afford the things they need and to save money.

- Home ownership plays a key role here—but for many younger Australians, the cost of buying a home is increasingly prohibitive.

Cathryn* runs her own boutique content and communications agency in Melbourne. The 43-year-old lives with her husband—an IT engineer—and their three-year-old daughter in a two-bedroom apartment in the inner-city suburb of Fitzroy. Yet despite being part of a double-income professional household, Cathryn believes her family is less financially secure than her parents would’ve been at a similar point in their adult lives. “I would definitely say my husband and I are financially worse off than my parents were at the same age,” she says.

On paper, Cathryn concedes the dollar amount of her household income would exceed that of her parents, who were able to rely on her father’s salary to support a family of four. But when she reflects on why she and her husband are more financially stretched, she is in no doubt of the reason.

“It comes down to housing costs and the cost of living,” she says. “My parents retired on the dot of their 60th birthdays because they hadn’t been paying a huge mortgage. It gave them a lot of freedom of choice. Whereas I think we'll probably be working until we’re at least 70 or 75.”

Increased financial challenges

Cathryn is hardly an isolated case. This year’s data from the Australian Unity Wellbeing Index—a 24-year study into the wellbeing of Australians, run in partnership with Deakin University—shows that almost half of Australians aged 18 to 54 feel financially worse off than their parents at the same age, compared to just 20 percent of people aged 55 and over. This financial insecurity has wide-ranging implications, with those who felt worse off also reporting lower levels of personal wellbeing.

But the drop-off is hardly surprising, given the data also shows that people aged under 55 are also more likely to put off paying for essentials like medicine or food due to financial pressures, and are less satisfied with their ability to afford the things they need. Younger Australians are also less satisfied with their ability to save money, making it even more difficult to get out of a financial hole.

The most hard-hit demographic? People aged between 25 to 44. This group—who are often in the “crunch years” of raising a family and buying a home—reported the lowest satisfaction with their ability to save money or afford the things they need.

The impact of home ownership

“I think interest rates probably have a lot to do with [these issues],” says the Australian Unity Wellbeing Index’s lead researcher, Dr Kate Lycett. “The cost of housing and thirteen consecutive rate rises have put a lot of people in financial hardship.

“People who don’t own a house are probably finding it hard to believe they’ll ever get there. This has significant intergenerational effects, because these people are at the age where they might be ready to start a family but are delaying that decision as a result.”

The latest Australian Unity Wellbeing Index data supports the view that housing and mortgage stress are some of the biggest factors behind this generational divide. It showed that only 7 percent of people aged under 55 were mortgage-free, compared to 61 percent of people aged over 55—and, notably, homeowners had significantly higher personal wellbeing scores than people who were still paying off their house, renting or living with their parents.

“If you don’t have help from the Bank of Mum and Dad, it’s almost impossible to think that you’re ever going to get on the property market,” says Kate. “We saw that people who were renting or had other living situations had lower wellbeing than people who owned a house. In particular, they had worse satisfaction with their future security. So all of these things have a big impact.”

A difficult path to financial stability

This age-based gulf in wellbeing is grimly inevitable in the current environment, concedes Esther Kerr, Australian Unity’s CEO of Wealth and Capital Markets. She believes that younger Australians face mounting obstacles to achieving financial stability, particularly compared to previous generations.

“Generally, they’re starting with higher debt because university costs a lot more, so they’re already behind. Interest rates are probably the same—in fact, my parents probably faced higher inflation at various points. But for my kids who are about to be working age, a ticket to play in the housing market is out of reach,” she notes.

“You used to be able to save for a house deposit in a fairly reasonable timeframe. Now it takes about 12. I wouldn’t have saved for a housing deposit if it was going to take me until I was 36—I’d be like: ‘Stuff that, it’s not logical.’”

This is particularly concerning given the important role asset ownership now plays in our financial stability. If you own a house, Esther points out, the price is likely to have increased. Similarly, if you have cash savings, you’ll have been able to capitalise on steepening interest rates. “If you are a borrower or living more hand-to-mouth without cash or savings sitting around, then you are on the wrong side of that,” she says.

Bridging that gap is more challenging than ever given the spiralling cost of living and the prohibitive cost of home ownership. “What we now have is a generation over 55 that typically own real estate and have savings, while the younger generations are on a hamster wheel that is just spinning faster and asset ownership is getting further and further out of their reach,” says Esther. “The gap has not just inflected, it’s now accelerating.”

*Not her real name

Disclaimer: Information provided in this article is of a general nature. Australian Unity accepts no responsibility for the accuracy of any of the opinions, advice, representations or information contained in this publication. Readers should rely on their own advice and enquiries in making decisions affecting their own health, wellbeing or interest. Interviewee titles and employer are cited as at the time of interview and may have changed since publication.